Average Annualized Outperformance of Companies Before and After First Year Becoming 1 of 10 Largest in US

Compared to Fama/French Total US Market Research Index, 1927-2019

Past performance is no guarantee of future results. Indices are not available for direct investments; therefore, their performance does not reflect the expenses associated with the management of an actual portfolio.

Stocks Measure Tomorrow, Not Today

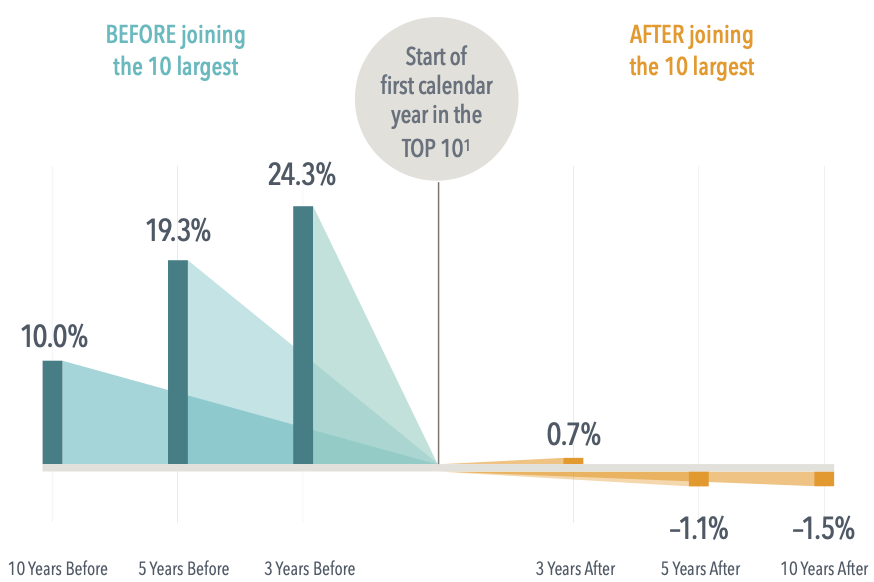

As companies grow to become some of the largest firms trading on the US stock market, the returns that push them there can be impressive. But not long after joining the Top 10 largest by market cap, these stocks, on average, lagged the market.

From 1927 to 2019, the average annualized return for these stocks over the three years prior to joining the Top 10 was nearly 25% higher than the market. In the three years after, the edge was less than 1%.

Five years after joining the Top 10, these stocks were, on average, underperforming the market—a stark turnaround from their earlier advantage. The gap was even wider 10 years out.

Intel is an illustrative example. The technology giant posted average annualized excess returns of 29% in the 10 years before the year it ascended to the Top 10 but, in the next decade, underperformed the road market by nearly 6% per year. Similarly, the annualized excess return of Google five years before it hit the Top 10 dropped by about half in the five years after it joined the list.

Expectations about a firm’s prospects are reflected in its current stock price. Positive news might lead to additional price appreciation, but those unexpected changes are not predictable.