Investing in an Uncertain World

There’s a misconception in the markets: value stocks have lost their vigor. Value stocks have underperformed growth stocks over the past decade. In the US, the annualized compound return has been 12.9% for value stocks, or those trading at a low price relative to their book value. That contrasts with 16.3% annualized compound return for growth stocks, or those with a high relative price.

Value underperforming growth by 3.4% a year over a decade is disappointing. But one question investors might ask themselves is, how do the returns for value and growth stocks over the past decade compare with their long-term averages?

Looking at returns for the US value and growth indices separately, we see growth’s annualized compound return of 16.3% over the 10-year period ending June 2019 was much higher than its return since July 1926, at 9.7%. On the other hand, value performance over the past decade has been more or less in line with its historical average: 12.9% vs. 12.7%. Value has performed similarly to how it has historically behaved. It is growth stocks that have had very good recent returns relative to the long-term history. Investors maintaining an emphasis on growth stocks may be hoping this departure from the trend will endure, despite the historical long-term averages.

A Quick Comeback

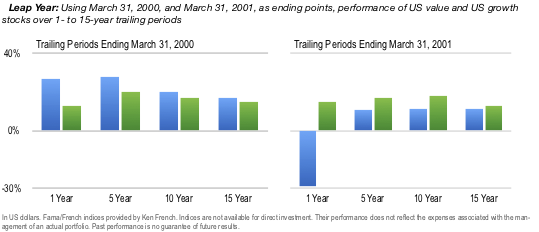

While stock returns are unpredictable, there is precedent for the value premium turning around quickly after periods of sustained underperformance. For example, some of the weakest periods for value stocks when compared to growth stocks have been followed by some of the strongest. On March 31, 2000, growth stocks had outperformed value stocks in the US in every 1 to 15-year period. As of March 31, 2001—one year later—value stocks regained the advantage over every one of those periods.

The theoretical support for value investing is longstanding—paying a lower price means a higher expected return. However, realized returns are volatile. A 10-year negative premium, while not expected, is not unusual. But history also tells us that changing course after a disappointing spell for known premiums can lead to missed opportunities. When those drivers of outperformance have turned around in the past, steadfast investors have been rewarded. A key to successful long-term investing is sticking with your approach, even through difficult periods, so that you are there for the good times too