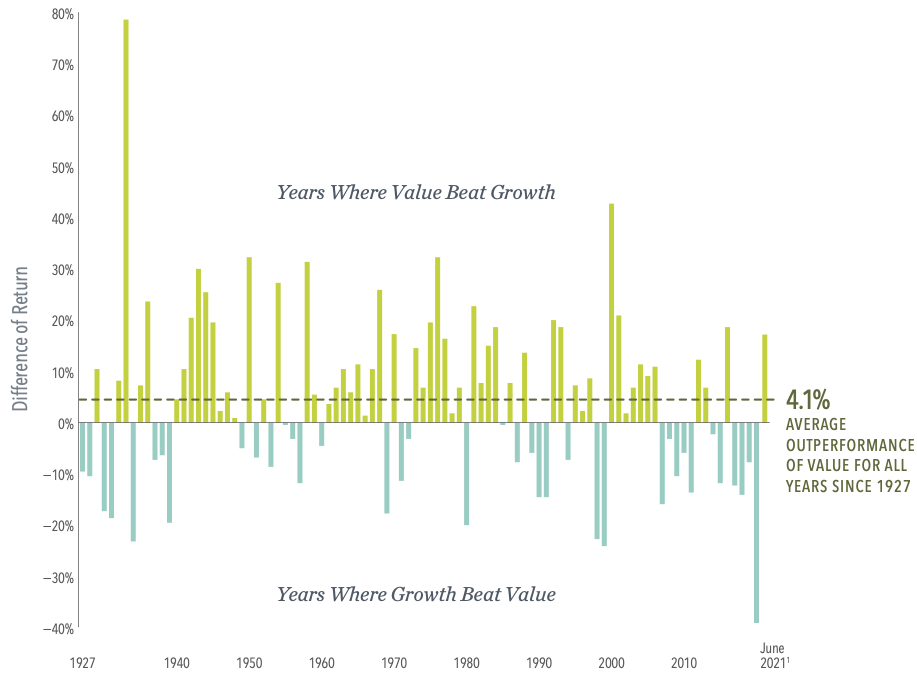

Yearly Observations of Premiums: Value minus Growth: US Market January 1927—June 2021

Past performance is no guarantee of future results. Investing risks include loss of principal and fluctuating value. There is no guarantee an investment strategy will be successful. Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio.

Evidence-Based Investing

Historically, value stocks have outperformed growth stocks in the US, and the outperfor- mance in a given year has often been striking.

Data covering nearly a century backs up the notion that value stocks—those with lower rela- tive prices—have higher expected returns.

Value premiums have often showed up quickly and in large magnitudes. For example, while the average annual value premium since 1927 hasbeen 4.1%, in years when value outperformed growth, the average premium was over 14%.

There is no evidence investors can reliably pre- dict when value premiums will show up. Rather, a consistent focus on value stocks is essential to capturing these outsize value premiums when they do appear.

Logic and history support a commitment to val- ue stocks so investors can be positioned to take part when those shares outperform in the future